Next: Testing Hypotheses

Up: Statistical Definitions

Previous: Sample Distributions

Contents

Subsections

Some definitions

Even efficient estimators will have some error when they estimate

the value of a population parameter. In many cases it is better to know

an interval within which the population parameter can be found. This

type of estimate is termed as an interval estimate, ie we say

that the population parameters lies within the interval

Some features of interval estimates

Since

has a sampling distribution centered at

has a sampling distribution centered at  (the

population mean) it has a variance smaller than other

estimators of . Furthermore since the variance of

is

defined as

(the

population mean) it has a variance smaller than other

estimators of . Furthermore since the variance of

is

defined as

, the variance

decreases with larger sample sizes. Thus

, the variance

decreases with larger sample sizes. Thus

is the best point

estimate of

is the best point

estimate of

Considering interval estimates we know that the Central Limit

Theorem says that the sampling

distribution of

is approximately normal with mean

and standard deviation

and standard deviation

. Thus if

. Thus if

is the z value above

which we get an area of

is the z value above

which we get an area of

then we can write

then we can write

and since Z is defined as

we can substitute and manipulate to get

Essentaially this says that if

is the mean of a

random sample of size  taken from a population with mean

and standard deviation

taken from a population with mean

and standard deviation  then the

then the

confidence interval for is given by

Thus the values of

confidence interval for is given by

Thus the values of

and

and

are the left

and right sides of the inequality.

are the left

and right sides of the inequality.

Thus for the mean we can say that if

is an

estimator of then we can be

sure that

the error (ie

) will not exceed

) will not exceed

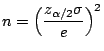

The number of members in a sample required to achieve a

confidence level for an error  (ie

sure that the error will not exceed

) is given by

(ie

sure that the error will not exceed

) is given by

When we have a sample from a normal distribution with an unknown

standard deviation then the variable defined as

has a t distribution with

degrees of freedom. Proceeding as above we can conclude that if

and

degrees of freedom. Proceeding as above we can conclude that if

and  are the sample mean and standard deviation of a

sample from a normal population with unknown variance then a

confidence interval for is given by

where

are the sample mean and standard deviation of a

sample from a normal population with unknown variance then a

confidence interval for is given by

where

is a t value with

is a t value with  degrees of freedom.

degrees of freedom.

An important feature is when is known we can use the Central Limit

Theorem (ie a normal

distribution) and when is

unknown we use the sampling distribution of T (ie a t

distribution). In many

cases when is unknown and  can be used instead of

to give the interval

can be used instead of

to give the interval

This is termed as the large sample confidence interval

We know that the variance of the estimator

is

The standard deviation of

is also termed as the

standard error. Thus confidence intervals can also be written

as

- Width of the confidence interval depends on the standard error of

the estimate

- Alternatively the width of the confidence interval depends on the

quality of the estimate

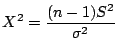

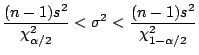

When using  as an estimator for the population

as an estimator for the population

we

can get an interval estimate of

by the statistic

which has a

we

can get an interval estimate of

by the statistic

which has a  distribution with degrees of freedom (when

the samples are taken from a normal population). Rearranging and

proceeding as before we get

distribution with degrees of freedom (when

the samples are taken from a normal population). Rearranging and

proceeding as before we get

Next: Testing Hypotheses

Up: Statistical Definitions

Previous: Sample Distributions

Contents

2003-08-29